The U.S. stock-market rally that marked the first half of 2023 continues into the second half, leaving bullish investors clinging to the optimism that has helped the technology-heavy Nasdaq 100 index advance by 42% for the year to date, while bears are trying to time the point when momentum fizzles out and the trend shifts to the downside.

The dichotomy between the so-called stock-market bulls — who are optimistic and buy shares in the hope that stock prices will rise — and bears — who believe that the market is headed downward and may attempt to profit from a decline in stocks — has grown wider.

“[It’s] almost resembling a political landscape where each side looked at the other with anger and resentment, unable to find common ground,” said Liz Young, head of investment strategy at SoFi, in a Thursday note. “Understandably so, given the plethora of conflicting data — not the least of which is the unexpectedly feverish stock-market rally in the face of leading economic indicators and bond market signals that are clearly waving a red flag.”

U.S. stocks extended the rally this week after encouraging inflation readings bolstered the chances that an end to the Federal Reserve’s interest rate hikes might be in sight, while odds of a soft landing, in which inflation returns to close to the central bank’s 2% target without a recession, are improving.

The S&P 500

SPX,

on Thursday cleared the 4,500 mark for the first time since April 2022 while rising to a fresh 15-month high. For the week, it has risen 2.4%, while the Nasdaq Composite

COMP,

has advanced 3.2% and the Dow Jones Industrial Average

DJIA,

has gained 2.3%, according to FactSet data.

See: Inflation in the U.S. has cooled off significantly. Great. Here’s what’s not so great.

Market analysts told MarketWatch that the debate between bulls and bears will not cease and the sentiment will not turn “full-on bullish” until uncertainties around monetary policy, economic indicators and Treasury yield-curve inversions are resolved.

“We’ve still got a monetary tightening cycle that may or may not be done yet. We’ve got leading economic indicators that are flashing contraction — there’s a lot of different signals out there, including yield-curve inversions, that are still saying we are not out of the woods,” Young said in a follow-up interview on Friday. “The debate will continue and I happen to be on the more cautious side of this, particularly with valuations at this level.”

“This means that for now, markets are likely to take two steps forward, one step back, unless an event comes along to turn investor sentiment negative again, like most of last year,” said Melissa Brown, managing director of applied research at Qontigo.

The surge in valuation of megacap technology stocks including Nvidia Corp.

NVDA,

Meta Platforms

META,

Alphabet Inc.

GOOGL,

has pushed the S&P 500 more than 17% higher so far this year amid the growing optimism surrounding artificial intelligence (AI). However, there is a risk that investors are paying “inflated valuation” for a stock based on AI enthusiasm, but if they do not get the “gratification” from it in the next 12 months, the valuation may not look attractive any more, said Young.

“When you buy stocks, you typically buy them on a forward 12-month earnings expectation basis, and although AI may very well be a completely transformative theme that ripples through different industries, it’s probably not going to change it [technology landscape] entirely by the end of this year,” she said. “So what could go wrong is the timeframe expectation.”

See: Nasdaq is making a big change to its most popular index. Here’s how it might impact your portfolio.

Brown of Qontigo also pointed to the current volatility in the stock market, which has fallen substantially since late March when the concerns about the banking sector dissipated after the sudden collapse of Silicon Valley Bank. The CBOE Volatility Index

VIX,

was at 13.31 on Friday, after recently dropping to its lowest level in more than three years. In general, a VIX reading below 20 suggests a perceived low-risk environment, while a reading above 20 is indicative of a period of higher volatility.

However, Brown said her models show that there is an increasingly wide gap between a fundamental model — which analyzes market volatility based on macroeconomic conditions — and a statistical model — which lets the data tell where the volatility is.

“The statistical model forecasts much higher risk than the fundamental model and this is the first time this has happened in at least six years and probably longer. So what that tells us is that there’s volatility lurking somewhere… it is bubbling under the surface,” Brown told MarketWatch via phone on Friday.

Looming lack of liquidity is another large concern as investors are now “significantly overbought” relative to liquidity, especially among megacap growth stocks, said Raheel Siddiqui, senior research analyst of global equity research at Neuberger Berman.

Siddiqui, said in his third-quarter equity-market outlook, that investor euphoria tends to evaporate as liquidity dries up, which is expected to happen soon thanks to a potentially historic withdrawal in coming weeks. He was referring to the Fed’s plan to shrink its balance sheet each month, otherwise known as quantitative tightening, the Treasury’s issuing of new debt to replenish the Treasury General Account after Congress raised the debt-ceiling, and the European Central Bank’s plan to pull €477 billion in TLTRO financing out of the banking system.

See: ‘Potent liquidity squeeze’ threatens stock market once debt-ceiling deal is done

“In our view, this could spell bad news for equities in the near term,” said Siddiqui.

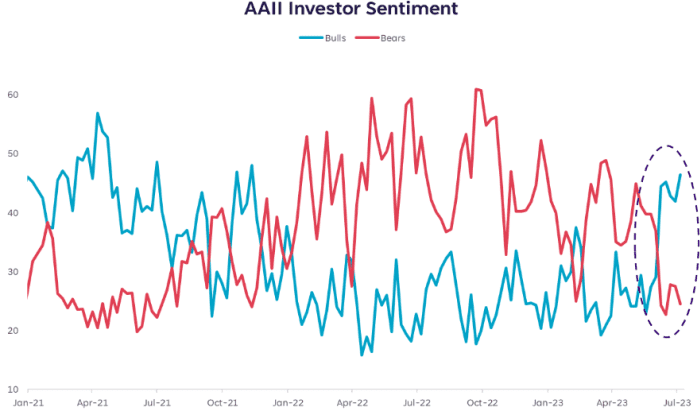

Stock-market optimism decreased but remains above average for the sixth consecutive week in the latest American Association of Individual Investors (AAII) Sentiment Survey. Neutral sentiment and bearish sentiment both increased in the week to Wednesday.

However, Young at SoFi said there has been a significant “flip-flop” from investors who were bearish and persistently bearish and have moved over into a bull camp. “Although the absolute level of bulls vs. bears in the chart doesn’t appear to be at extremes, the almost instantaneous reversal in the two is quite extreme,” she said (see chart below).

SOURCE: SOFI, BLOOMBERG

“Generally, large and swift moves can be followed by large and swift moves back in the other direction as markets and investors attempt to settle on some sort of middle ground,” Young said.