The U.S. economy hasn’t stumbled yet, even through the Federal Reserve has jacked up interest rates to a 22-year high.

That’s a key factor driving a “grab for yield” in stocks and riskier corporate bonds, according to Mizuho Securities.

The absence of a broad credit crunch following the failures of Silicon Valley Bank and Signature Bank in March also “suggests it is safe to grab yield, especially if you believe the Fed will be successful in returning inflation to its 2% target in relatively short order, avoiding the need for a recession and/or a significant deterioration in the labor market,” Thaddeus Strobach, a Mizuho high yield strategist, wrote in a Monday note to clients.

As evidence of this, yields in the riskiest $1.5 trillion junk-rated portion of the U.S. corporate-bond market climbed to a peak of roughly 8.9% in March, according to Fed data, after the collapse of several regional lenders raised concerns about a larger banking crisis.

Yields lately have been closer to 8.5%, even though the Fed has continued to bump up its policy rate to its current 5.525%-5.5% range since March to ensure that receding inflation doesn’t flare up again.

Stocks have slumped in August as long-term Treasury yields have surged, but the S&P 500

SPX

and Nasdaq Composite Index

COMP

booking their first gain in five sessions on Monday.

Goldman Sachs analysts recently said they think there’s room to add to exposure to equities if the U.S. economy stays on a path to a soft landing.

The benchmark 10-year Treasury yield

BX:TMUBMUSD10Y

was back to its highest level since Nov. 6, 2007 on Monday, near 4.339%, according to FactSet. The rate makes up a portion of the return offered by junk bonds, plus a spread or premium to help compensate investors for default risks. The spread on the ICE BofA US High Yield Index was last pegged at 4%.

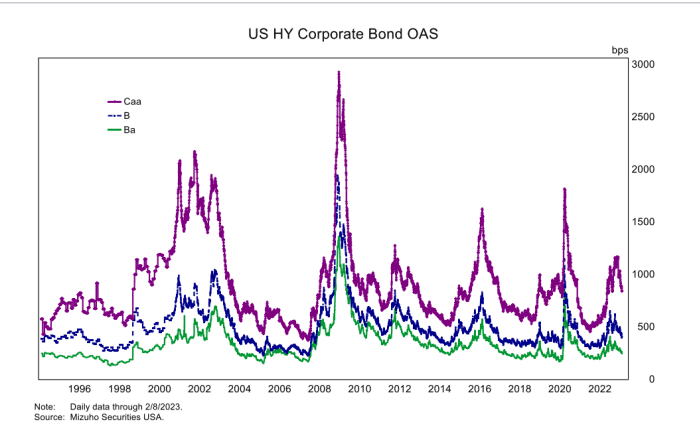

Falling junk-bond spreads, even for the riskier Triple C class of junk bonds (see chart), point to a willingness among investors to bet on debt-laden companies while getting paid less.

Junk-bond spreads are falling as investors grab for yield.

Mizuho Securities USA

“Spreads have narrowed even as the speculative default rate has risen from an exceptionally low level,” Strobach wrote. “However, default rates, at 1.43% in August, remain well below what is implied by the tightening standards in the Fed’s senior loan officer survey.”

This comes as U.S. high-yield funds saw negative $8.7 billion in outflows this year as a percentage of assets under management, according to Goldman Sachs analysts.

Still, Strobach said a sideways movement in the U.S. dollar

DXY

also adds to the grab-for-yield strategy, while he expects oil prices, including the price of the U.S. benchmark West Texas Intermediate crude

CL00,

which is near $80 a barrel, to remain near the recent upward end of their recent range.

The U.S. junk-bond index has long been heavily weighted to the energy industry.

Related: Stocks might not get trampled by central bank ‘elephants.’ We were wrong, says UBS CIO