How bullish is that the S&P 500

SPX,

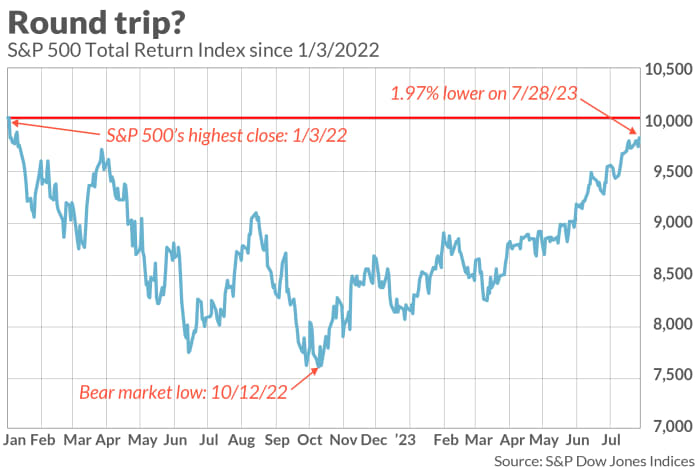

is close to completely recovering from its 2022 bear market losses? The benchmark U.S. stock index with dividends reinvested (total return) is just 2.0% below its January 2022 all-time high. Even a modestly good week in the stock market could push this benchmark over the top.

If this does happen soon, the recovery from the 2022 bear market would be one of the quickest in history. It’s been less than 10 months since the S&P 500’s bear market low last Oct. 12.

Unfortunately for the bulls, the market’s future can’t be judged on the speed of this recovery. Quick recoveries don’t necessarily presage better subsequent stock market performance than longer recoveries.

To reach this conclusion, I analyzed all bear markets since 1900 in the calendar maintained by Ned Davis Research. In each case, I calculated how long it took for the U.S. stock market to rise above the level at which it stood when that bear market began. I then measured the correlations between that recovery time and the stock market’s performance over the one-, two- and three years subsequent to that recovery.

None satisfied traditional standards of statistical significance. Sometimes, as was the case after the February-March 2020 bear market, a quick recovery time (just five months in that case) was followed by strong subsequent market performance. But the market also performed extremely well subsequent to the four-year recovery from the 2007-2009 Global Financial Crisis.

This result is what we should expect, given the stock market’s efficiency. One of the hallmarks of that efficiency is that the market is forward-looking. How it will perform in coming months is a function of whether the news will be better or worse than currently expected — not how the stock market performed prior to now.

Imagine for a moment if a quick recovery time did increase the odds of strong subsequent performance. In that case, traders would rush in to buy stocks, and by doing that would bid up prices until the market’s expected future return is no better than average.

The bottom line? We can all celebrate the stock market’s recent strength. But celebration is not an investment strategy. Our job as investors will return to what it always is: analyzing whether the news is coming in better or worse than expected.

Mark Hulbert is a regular contributor to MarketWatch. His Hulbert Ratings tracks investment newsletters that pay a flat fee to be audited. He can be reached at mark@hulbertratings.com